HIGH COURT APRIL 2025 WEEKLY ROUNDUP | Taman Singh Sonwani’s Bail; Murshidabad Violence; Influencers’ Free Speech; Chandola Lake Demolition; and more

A quick legal roundup to cover important stories from all High Courts this week.

Bringing you the Best Analytical Legal News

A quick legal roundup to cover important stories from all High Courts this week.

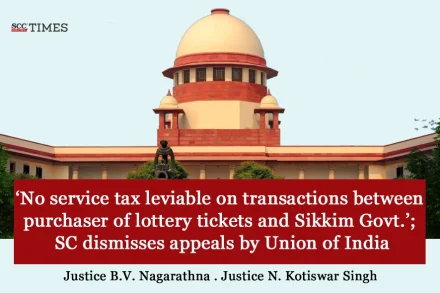

Services provided by an advocate or a Partnership firm of advocates providing legal services to any person other than a business entity and a business entity with a turnover up to rupees ten lakhs in the preceding financial year are exempted from the levy of service tax.

“There being no agency and no service rendered by the respondents-assessees herein as an agent to the Government of Sikkim, service tax is not leviable.”

Advocates Act, 1961 — S. 24(1)(f) — Enrolment Fees: Charging of enrolment fees in excess of statutory stipulation under Advocates Act, 1961

Special leave petition – Exemption from filing the certified copy of the impugned order of the High Court

The assessee-appellant contended that they acted on principal-to-principal with both the customers (shipper) and the shipping line/airline. A freight forwarder may act as principal and raise invoice to the exporter on his own account, providing transportation of goods and is not acting as “intermediary”.

All the activities rendered by the appellant are undertaken during hosting the cricket matches alone and if there were no cricket matches played, then all these services become irrelevant.

The services were not received by the appellant regarding which invoices have been issued to the appellant’s other two addresses, other than the address for which service tax registration has been taken, is contrary to the contention stated by Revenue in the show cause notice. Therefore, the same is not sustainable in law.

The Tribunal noted that Rule 4A (1)(i) of Service Tax Rules, 1994 requires disclosure of service tax payable on the value of service provided, thus, it cannot include exempted services. Moreover, a proviso inserted to the Rule by an amendment cannot enlarge the scope of the provision, at best it is only clarificatory.

The Tribunal stated that for a place to fall within the ambit of a public place, the element of right of access of public was a necessary concomitant.

The Tribunal opined that both service provider and service recipient were government undertakings and cannot be said to have any intention to evade the tax payment.

The Tribunal opined that once the coal companies have charged sales tax/VAT at the appropriate rate on the sale of coal to appellant and in turn, appellant has charged sales tax/VAT to the consumers of coal, the transaction is one of sale/purchase and not of rendering service.

“It is very simple in the accounting standards that unless invoice is raised consideration is not collected. Therefore, it is very clear from the record that the appellant was not receiving any consideration from card companies.”

“The services like wireline logging, perforation and other wireline related services involving mechanical jobs which were undertaken by appellant at the time of drilling an oil well are integrally connected with the mining of oil or gas and have a direct nexus with the drilling of a well.”

Criminal Law — Criminal Trial — Proof — Burden and Onus of proof — Recourse to S. 106 of the Evidence Act

As the service tax needs to be computed in terms of Rule 2A of the Service Tax (Determination of Value) Rules, 2006 and as the assessee has not opted for the composition scheme, the matter is remitted back to the CESTAT for re-computation of the demands.

The Delhi High Court held that the Commissioner of CGST and Central Excise cannot continue the proceedings for adjudication of the impugned show cause notice, after the lapse of thirteen years.

by Tarun Jain†

Cite as: 2023 SCC OnLine Blog Exp 28

The Delhi High Court set aside the demand for service tax of Rs. 56 crores against MTNL holding that the surrender of any right to use the spectrum before 14-5-2016, the date on which the Finance Act, 2016 came into force, will not be chargeable to service tax.

Criminal Procedure Code, 1973 — S. 427 — Consecutive or concurrent running of sentences: Normal rule is that such subsequent sentence shall